If you are working with a financial advisor (whether of the human or the robo variety), you can be sure they are getting paid for the advice. Investment fees and other charges are simply a part of investing.

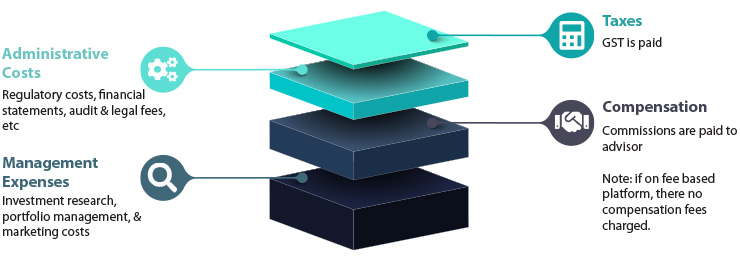

Investment firms or registered investment advisors charge fees to cover the costs associated with administering investment products, operating your account, making transactions on your behalf, or offering advice.

Why do investment fees matter?

Investment fees impact the overall returns (or losses) in your portfolio, so it is important to know what they are. When you understand your fees and their impact, you can evaluate the true cost and suitability of the investments in your portfolio and the services you receive from your investment advisor.

What type of fees are there?

The financial marketplace has countless different investments available and you have a choice on how you pay the fees associated with them. Some fees are embedded in the product itself, like a management expense ratio (MER) of a mutual fund, others may be charged outside the investment as part of a fee-based platform.

Built in fees

These are fees (also called MERs or bundled fees) associated with mutual funds and ETFs and are charged by the fund manager, not your advisor. These are the fees that are embedded in your funds (such as a mutual fund or ETF) and are the expenses associated with running and managing it. These expenses are deducted from the fund’s performance; therefore, when you see a posted rate of return of, for example, of 3% and a fund fee of 2%, the fund actually had a total return of 5%. Therefore, the lower the fund fee, the more money goes into your pocket.

Fund fee breakdown:

According to Morningstar, the average MER (Management Expense Ratio) on an equity fund in Canada is 1.76%.2

According to a Morningstar report2, where they calculated the asset-weighted average Mutual Fund MERs in each distribution channel by broad asset class, the average fees were:

| Asset Class | Commission Based | Fee Based | Do-it-yourself |

| Domestic Core Bonds | 1.6% | 0.8% | 0.6% |

| Domestic Core Equity | 2.1% | 1.1% | 1.1% |

| Domestic Noncore Equity | 2.6% | 1.6% | 1.6% |

For the most part, ETFs are less costly than mutual funds. There are exceptions—and investors should always examine the relative costs of ETFs and mutual funds that track the same indexes. However—all else being equal—the structural differences between the 2 products do give ETFs a cost advantage over mutual funds.

Mutual funds charge a combination of transparent and not-so-transparent costs that add up. It’s simply the way they are structured. Most, but not all, of these costs are necessary to the process. Most could be a little cheaper; some could be a lot cheaper. But it’s nearly impossible to get rid of them altogether. ETFs have transparent and hidden fees as well—there are simply fewer of them, and they cost less.

If you combine active & passively managed mutual funds and ETFs, the average MER on an equity fund in Canada is 1.76%.3

Advisor Fees

Advisors are paid one of two ways: a commission from the built-in fees or a flat fee (no commission)

- The commission fees, as mentioned above, are built into the mutual fund or ETF, and are paid by the fund company to the advisor. In addition, commission fees, some advisors additionally add a another fee to the fund called a front- or back-end “load,” when buying or selling a fund. Up until 2022, there were also deferred sales charges (DSC) but these have since been banned in Canada by Canadian Securities Administrators (CSA).

- Alternatively, the flat fee (or fee-only service) does not collect a commission and instead, an annual fee is paid. This fee is negotiated at the beginning of your client-advisor relationship, and it pays for the cost of managing your overall portfolio and is usually a percentage of your assets under management, which can be anywhere between 0.6% – 1.3% depending on the total value of your investment. There are some brokers (usually a discount brokerage) that instead of charging a flat fee they apply a fee per trade but may also charge additional amounts related to the number of trades and the size and scope of the account.

The flat fees are typically used for investments that hold stocks, ETFs, bonds, etc or those portfolios that have higher trading volumes. Mutual funds held with this fee platform do not have compensation fees built in (as noted in the image above).

According to Advisory HQ4, the average financial advisory fees are between 0.59% to 1.18%, depending on how much money you have invested. Our fees, at Savanti Investment Team | PEAK Securities Inc. is 0.75% -1.1%.

Can I deduct investment fees from my taxes?

As Canadian taxpayers, we are always looking for opportunities to save our tax dollars so when comes to your investment fees, which can you deduct, and which can you not?

According to the Income Tax Act, a taxpayer may deduct fees that are charged for advice on the buying or selling of specific shares or securities, or for the administration or management of securities held by that taxpayer, provided that the fee amounts paid are reasonable.

Not tax deductible:

- The built-in fees embedded into your mutual fund and ETF (ie MER, etc).

- Advisory and other investment fees charged on registered assets (RRSP, TFSA, RRIF, LIRA, LIF, RESP, segregated funds, etc), regardless of the investments held

- Commissions to buy or sell investments

Fees that are tax deductible:

- The flat fee that an advisor charges for those investments held in non-registered investments.

- Fees to manage or take care of your investments or fees for certain investment advice, such a for a financial planner

If you pay your advisor a flat fee, you can find out exactly what you paid each year from your annual investment fee report, also known as the Annual Charges and Compensation Report.

Fees are important in the sense that any fee you pay takes away from the performance of your investment. It is important that you know how much you are paying in fees. If you are paying more than the average, you should question the value you are getting from higher fees. While there is some correlation that the lower fees you pay the better your long-term returns, don’t get caught up in focusing on fees alone. Evaluating mutual funds goes far deeper than analyzing and comparing MERs.

1 Canada Revenue Agency, IT238R2 ARCHIVED – Fees paid to investment counsel.

2 https://www.morningstar.ca/ca/news/190913/what-canadians-pay-for-mutual-funds-part-2.aspx

3 Morningstar Global Investor Experience Study: Fees and Expenses.

4 https://www.advisoryhq.com/articles/financial-advisor-fees-wealth-managers-planners-and-fee-only-advisors/#Investment-Management-Fees